🎧 IBR’s $15B Bridge Project Hides Toll Revenue Study Until 2027

Joe Cortright reveals details of the IBR’s toll revenue study, which is once again delaying bad news to get officials to move forward with project approval

Joe Cortright

City Observatory

The Interstate Bridge Replacement Program (IBR) is hiding its toll revenue study — which will show that tolls will have to be higher and provide less revenue for the $15 billion project. They’re delaying this bad news to get officials to move forward with project approval, and plan to stick us with the bill later on.

- IBR officials have told Oregon and Washington legislators that the project’s Investment Grade Analysis (IGA) — a rigorous, independent estimate of future toll traffic and revenues — will be delayed by more than a year, to June 2027.

- According to the project’s own December 2024 schedule, the key milestones — traffic and gross revenue forecasting and net revenue forecasting — were supposed to be completed in October 2025. They are now nearly six months overdue, with no firm completion date for those critical steps.

- This is the same playbook IBR used on its bloated cost estimate: officials repeatedly promised updates from January 2024 through December 2025, then waited until after both state legislatures had adjourned their 2026 sessions to reveal the project’s cost had more than doubled — from $5–$7.5 billion to $12–$15 billion.

- There’s an obvious reason for the delay: IBR staff have almost certainly already seen draft results showing that toll revenues will fall well short of the $1.25 billion they’ve been promising — and that hitting that target would require tolls far higher than they’ve been advertising.

- The whole point of an Investment Grade Analysis is that bond buyers, banks, and the federal government don’t trust state highway department traffic forecasts — because those forecasts are routinely and dramatically over-optimistic.

- We’ve seen this movie before. The 2013 Investment Grade Analysis for the Columbia River Crossing — which IBR’s own former director called “basically the same project” — cut projected future traffic nearly in half (from 178,000 to 95,000 vehicles per day) and nearly doubled the minimum toll (from $1.34 to $2.60).

- Four factors suggest IBR’s toll revenues will come in at the low end — or worse: bridge traffic is already down to 127,000 vehicles per day (not the 142,000 routinely cited in IBR materials); population and traffic growth have slowed; post-pandemic work-from-home has permanently dented commuter volumes; and 30-year interest rates have nearly doubled, shrinking how much can be borrowed against any given revenue stream.

- Once again this is the classic Robert Moses strategy: say anything to get the project started, and stick the public for whatever it ends up costing. IBR aims to get both states to make an irrevocable construction commitment before the IGA reveals the bad news on revenues and required toll levels.

- Legislators and the public deserve to see the Investment Grade Analysis before committing to a $15 billion project — not after.

Joe Cortright

Late last week, the Interstate Bridge Replacement Program (IBR) team told Oregon and Washington legislators that a long-promised and critical financial study for the Interstate Bridge project would be delayed by more than a year.

This is an ominous development. It signals that once again, IBR officials are hiding key information from the public and legislators. Apparently, IBR officials don’t intend to tell us how much money tolls will produce, or what toll levels will be–until after we make an irrevocable commitment to move forward with the $15 billion project.

This comes on the heels of a two-year-and-three month delay in releasing a new cost estimate for the same project, which saw its price more than double, from a range of $5 to $7.5 billion to between $12 and $15 billion. As we noted at City Observatory, IBR officials repeatedly promised a new cost estimate several times from January 2024 through December 2025, repeatedly concealing this higher cost estimate from legislators and the public, and waiting until after both the Oregon and Washington legislatures had adjourned their 2026 sessions to deliver the bad news that the project’s cost had doubled.

Now, after hiding the bad news on ballooning costs, they’re playing the same game by hiding bad news about revenues. One of the linch-pins of the project’s financing is a plan to start tolling the I-5 bridges between Portland and Vancouver. The study in question – called an “Investment Grade Analysis” is a rigorous estimate of how much traffic will use a tolled bridge, and how much revenue tolls can be expected to generate. There are many key questions: What’s the volume and trend of traffic on the bridges now? How will that change when traffic is tolled? What’s the outlook for future growth in traffic levels, especially with tolls? How high will the tolls have to be in order to provide hope for financing?

This question has taken on added significance as the project’s costs have doubled. IBR officials have been saying they expect tolling to provide about $1.25 billion in revenue to contribute toward construction costs. (Oregon and/or Washington would issue revenue bonds, backed by toll revenues, and pledge revenues–including regular annual increases in tolls–to try to raise the necessary funding. A key part of the study is combining the traffic modeling with assumptions about costs, growth and interest rates in order to estimate how much up-front money can be raised in bonds.

For a long time IBR has been saying that tolls will be in the $1.55 to $2.00 (minimum) and $3.65 to 4.70 (peak) for vehicles with annual increases of between 2.15 and 3.00 percent each year. The hope is that this will provide sufficient funds to support $1.25 billion in project costs, largely via bonds. That’s based on heroic assumptions in preliminary studies that traffic will grow robustly and not be much influenced by tolls. The whole reason for the “investment grade analysis” is that banks, bond buyers and the federal government do not trust the promotional forecasts generated by and for state highway departments to be an accurate predictor of future traffic and revenues. That’s why they insist on preparation of the “investment grade” study.

IBR officials claim – completely falsely – that the investment grade forecast is somehow a “worst-case” scenario, that can’t and shouldn’t be used to predict actual levels of future traffic on a tolled bridge or highway. That claim is completely untrue. The investment grade analysis is more detailed, more rigorous and more independent than the forecasts prepared for the EIS. It also turns out, in practice, that if anything, even Investment Grade analyses tend to over-estimate traffic on tolled facilities. There are plenty of examples of toll roads and bridges that have failed to meet investment grade forecast numbers; Nearby, for example, tis the toll-financed Tacoma Narrows Bridge, which has never met its investment grade revenue forecast. The conservative “investment grade study” for that project predicted that traffic on the bridge would grow at an annual rate of 1.7 percent per year after the capacity of the bridge was doubled. In fact, through 2019 (i.e. prior to the pandemic) actual traffic growth was only about a third that fast (traffic up 0.6 percent per annum), and has been even lower through 2025.

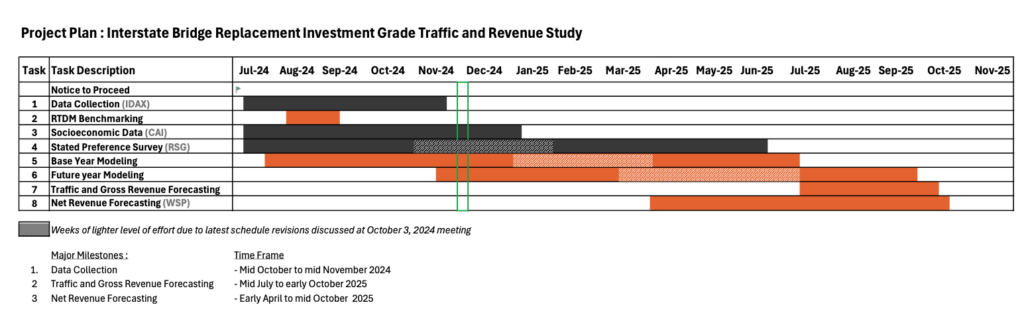

The Investment Grade Analysis was supposed to be done nearly six months ago

The traffic modeling and net revenue figures were supposed to be done October 2025, according to the project’s December 2024 schedule. Also, in a 2024 “fact sheet” IBR staff said that the Investment Grade Analysis would be done and toll rates would be adopted by the end of 2025. According to an email (reproduced below) to Washington State Representative John Ley, IBR officials have extended the time for the study for another full year, to June, 2027, and simply aren’t saying when the key milestones–“traffic and gross revenue forecasting” and”net revenue forecasting” will be completed.

Graphic courtesy Stantec: IGA Schedule. Source: Email: Dasigi, Shalini RE: Monthly IBR Level 3 T&R Study Status Update December 12, 2024 at 9:00 AM PST (via public records request)

Graphic courtesy Stantec: IGA Schedule. Source: Email: Dasigi, Shalini RE: Monthly IBR Level 3 T&R Study Status Update December 12, 2024 at 9:00 AM PST (via public records request)

As a result, project leaders, legislators and the public will continue to be in the dark about how high tolls will be, how much money they will contribute toward project costs, and how much traffic will divert to (and congest) the parallel I-205 freeway.

Why the delay?

There can be no doubt that IBR staff have seen at least the draft versions of the Investment Grade Analysis, including rough estimates of net revenues, and the amounts of debt such revenue streams would support. The work on the $2.3 million investment grade report, according to their own reporting, is 75 percent complete. The only reason for delay is that there is more bad news. It’s a virtual certainty that the amount of money that would be provided by the levels of tolls they’ve been talking about isn’t going to be enough to generate the hoped for $1.25 billion.

Therefore, it seems certain that that overall revenue number is much lower than they had hoped, and that getting a higher revenue number will require much higher tolls than they have been advertising. They are no doubt concerned that, coming on the heels of the new cost estimate, this will make the project even more unpalatable.

Hence what appears to be their plan: getting the two states to commit to the project *before* the full Investment Grade Analysis. That is irresponsible and reprehensible. Those responsible for this project–and those who will be asked to pay the bill – need to insist that the findings of the Investment Grade Analysis be released, immediately. Even if they are not “final,” the IBR and its consultants have no doubt of preliminary estimates that show the likely ranges of toll revenues, toll rates to be charged, and attendant traffic levels. The public’s leaders and the public need this information before the project goes forward, not after.

The IBR team and its consultants are painting their bosses (and the public) into a corner: once you start construction, you will be bound to pay whatever the cost is. And also, no one should buy the fiction that a subcommittee composed of members of the Washington and Oregon transportation commissions will “determine the toll rates.” The financial consultants will present a number, and say, if you want $1.25 or $1.5 billion from tolls, you must set the tolls at the rates they have determined. The commission’s choice will be take it or leave it–or find other money to cover what they had hoped to get from tolls.

A delay means less revenue is coming from tolls – and likely higher tolls as well

There are at least four good reasons to think that Investment Grade Analysis, when it is finally made public, will show that the net toll revenues from the project will be at the low end of the range IBR has been assuming (and that the toll rates will be at the high end).

First, according to official ODOT traffic counts, traffic on the I-5 bridges is down — 127,000 vehicles daily, not the 142,000 daily figure regularly mentioned in IBR press materials. Traffic levels now on the I-5 bridges are now no higher than the were two decades ago, and this gives the projections a lower base of traffic – and therefore revenue – from which to build.

Second, regional population growth and traffic growth have both slowed, meaning that in the future, we can expect much less traffic than was assumed in the wildly optimistic EIS forecasts. The early traffic studies done for the project simply failed to include the effects of post-pandemic shifts to work-from-home, which have continued to put a serious dent in commuter traffic.

Third, it seems likely that the IGA estimates will show traffic is much more sensitive to tolling that assumed in the EIS, and the earlier Level 2 study, which would depress revenue even further – and mean more diversion to I-205, as well as much less need for expanded capacity on I-5. The last IGA, done for the Columbia River Crossing, showed that travelers had a much lower “value of time” than the two DOT’s assumed, meaning that traffic was much more sensitive to tolls, with higher tolls producing less revenue and more traffic diversion than hoped for.

Fourth, interest rates have gone up: the benchmark thirty-year t-bill rate has nearly doubled from less than 2.5 percent a few years ago to nearly 5 percent now, and looks to be higher in the future. Higher interest rates decrease the amount of current capital expenditures than can be financed from the stream of expected future toll revenue.

IBR officials now say that the $1.25 billion contribution to project costs from tolling is just a “placeholder” value, and that they’re looking at alternatives to generate even more revenue. Back in the day when project costs were said to be in the $5 to $7.5 billion range, then-IBR Administrator Greg Johnson frequently said that tolls would provide “about a third” of project financing. And last session, the Washington Legislature approved a vague but substantial increase in WSDOT’s borrowing authority for the project. The trouble is that the only way to get more revenue is to charge even higher tolls. At some point, toll levels get so high that they don’t generate additional net revenue because they significantly reduce traffic.

We’ve been down this road before: CRC’s Investment Grade Study doubled minimum tolls

Keep in mind that, as the former IBR administrator said, the Interstate Bridge project is “basically the same” as the failed Columbia River Crossing. In 2013, after years of delay, ODOT finally got an “investment grade analysis” of the CRC project, which said that earlier projections were wildly over-estimated, and that as a result, the bridge would carry vastly less traffic, and tolls would need to be much higher. The Investment Grade study called for increasing all tolls and nearly doubling the minimum toll from $1.34 to $2.60. The Oregon and Washington highway departments prepared traffic and toll estimates for the Columbia River Crossing’s Final Environmental Impact Statement published in 2011. Those estimates were that the I-5 bridges would carry 178,000 vehicles per day in 2030, and that minimum tolls would be $1.34 to pay for about one-third of the cost of the project. The Investment Grade Analysis for this project, prepared by CDM Smith on behalf of the two agencies in 2013 estimated that in 2030, the I-5 bridges would carry just 95,000 vehicles per day in 2030, and that tolls would be a minimum of $2.60 each way in order to cover a third of project costs. In short, the initial highway department estimates overstated future traffic levels by double, and understated needed tolls by half.

Results of the Investment Grade Analysis of the Columbia River Crossing in 2013: Traffic estimates slashed almost in half, minimum tolls nearly doubled

The starkly different figures in the investment grade analysis called into question the size of the project, which was predicated on the exaggerated highway department forecasts. If a tolled bridge would carry dramatically fewer vehicles than the existing bridge, there was no justification for building an expensive wider structure and approaches. The billions and billions spent expanding capacity on the bridge and approaches would be wasted because fewer vehicles would use it, essentially forever.

Also read:

- POLL: Did the Clark County Council make the right decision by rejecting the auditor authority proposal?

The 3-2 council vote rejected giving the auditor’s office power to write financial impact statements for ballot measures.

The 3-2 council vote rejected giving the auditor’s office power to write financial impact statements for ballot measures. - Opinion: Hospital price transparency is good, but its impact will be limited

Washington still shields hospitals from competition through certificate-of-need laws other states have repealed.

Washington still shields hospitals from competition through certificate-of-need laws other states have repealed. - Opinion: Washington tax collections are running below forecast as the economy softens

Washington’s tax collections are $135.4 million behind forecast since February as employment and revenue both slip.

Washington’s tax collections are $135.4 million behind forecast since February as employment and revenue both slip. - Opinion: Washington’s Attorney General offers strong defense of signature gatherers’ rights

AG Nick Brown urges 39 county prosecutors to protect signature gatherers from harassment and theft.

AG Nick Brown urges 39 county prosecutors to protect signature gatherers from harassment and theft. - Letter: The IBR’s concrete obscenity

Bob Ortblad argues $17.7 billion buys one extra lane for five miles — and 30 years of debt for future generations.

Bob Ortblad argues $17.7 billion buys one extra lane for five miles — and 30 years of debt for future generations.