Chris Corry addresses one of the biggest questions that has arisen from the new rules for the Washington capital gains income tax

Chris Corry

Washington Policy Center

As the state begins developing new rules for the Washington capital gains income tax, various questions are being raised on the details of this new tax and how to apply the domicile rules correctly.

One of the biggest questions that has arisen is how Washington defines domicile. While the rules are still being drafted, tax attorneys at Lane Powell have created an eight-page checklist of factors related a taxpayer’s domicile.

While it would seem excessive to need an eight-page list, the domicile rules by the Department of Revenue are very presumptive of Washington domicile and require significant proof on the taxpayer’s part to prove they are no longer domiciled in the state. This creates complex scenarios for taxpayers.

As noted in the article:

“With respect to gains from the sale of tangible personal property, if the property is moved out of Washington at least two years prior to the sale of the property, the gains will not be allocated to Washington. In this case, the two years include the current taxable year and the immediately preceding taxable year.”

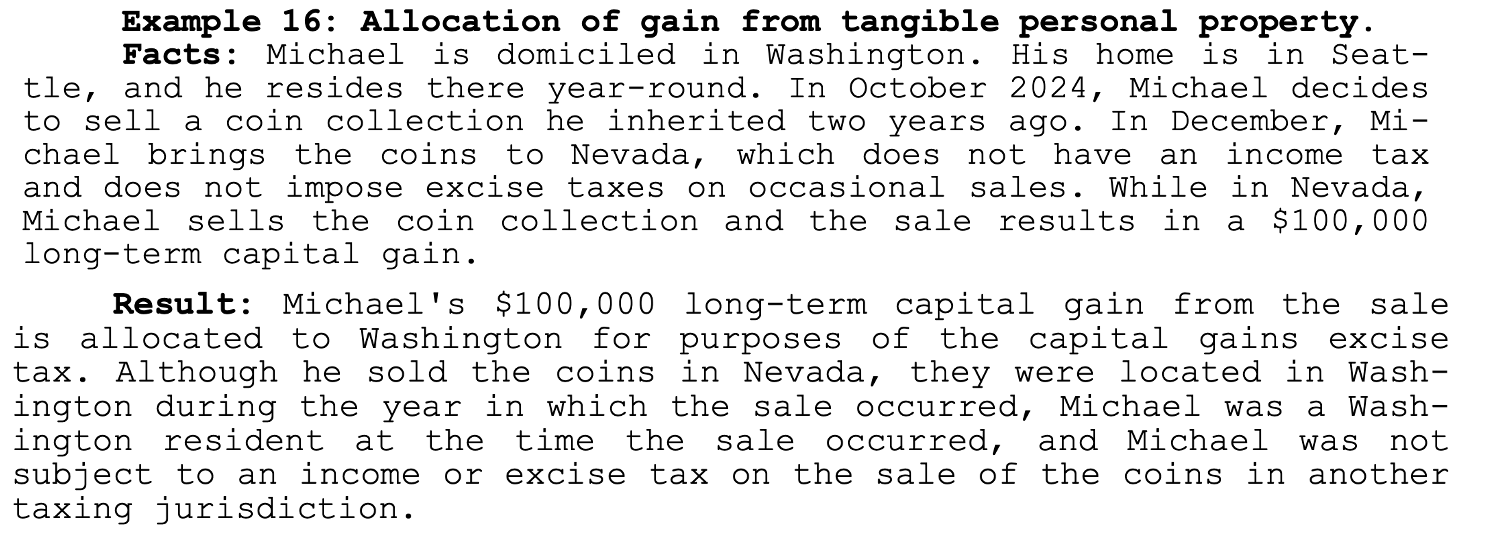

The example cited in the initial rulemaking was a Washington-domiciled resident selling coins in Nevada.

For the above example, to not incur the capital gains tax, the coins must be moved out of the state for two years before being sold. How Washington can apply an “excise tax” on a transaction outside its borders remains to be answered.

The guidance for clearing this domicile hurdle is complex. Per the authors:

“The key to an easy/favorable resolution in allocating long-term gains from intangible property is clear and convincing evidence that you have abandoned your Washington domicile with the burden on the party asserting the change, which is usually the taxpayer. To change domicile, a taxpayer not only needs to leave Washington but also must establish a new domicile. Completing this checklist and maintaining (in readily accessible files) evidence of all actions taken, including printouts of computer pages and emails, can help with both the assessment of the taxpayer’s domicile and carrying the burden of proof if there is a dispute with the tax authorities.”

The article and checklist can be found here.

Chris Corry is the director of the Center for Government Reform at the Washington Policy Center. He is also a member of the Washington State House of Representatives.

Also read:

- Letter: ‘This is the worst thing that ever happened to the region’

A Hayden Island resident Sam Churchill is criticized in a letter calling the $14 billion Interstate Bridge Replacement project a “boondoggle” that destroys local businesses.

A Hayden Island resident Sam Churchill is criticized in a letter calling the $14 billion Interstate Bridge Replacement project a “boondoggle” that destroys local businesses. - Opinion: Sheriffs fight back

Four county sheriffs are suing to block a new law giving a governor-appointed board power to decertify and remove sheriffs, bypassing voter oversight in Washington.

Four county sheriffs are suing to block a new law giving a governor-appointed board power to decertify and remove sheriffs, bypassing voter oversight in Washington. - Opinion: The growing gap between public voice and political power

Todd Myers describes how large-scale protest and sign-ins often fail to sway state leaders, and argues authentic influence is most likely found through local action.

Todd Myers describes how large-scale protest and sign-ins often fail to sway state leaders, and argues authentic influence is most likely found through local action. - Opinion: Who is winning the race for affordable power?

Hydroelectric power keeps Washington competitive, but new laws and carbon pricing are driving up electricity costs for residents each year.

Hydroelectric power keeps Washington competitive, but new laws and carbon pricing are driving up electricity costs for residents each year. - Opinion: Half the road, full stop – Understanding pedestrian right-of-way

Doug Dahl explains how Washington’s law requires drivers to stop when a pedestrian is within one lane of their half of the road, not just when directly in front.

Doug Dahl explains how Washington’s law requires drivers to stop when a pedestrian is within one lane of their half of the road, not just when directly in front.